So, you’ve made the big move—or you’re planning to. Welcome to Dubai, one of the world’s most dynamic cities for expats. But before you get swept up in skyscrapers, brunches, and beach weekends, there’s one thing you need to sort out fast: your essential cards.

Whether you’re here to work, launch a business, or simply enjoy the tax-free lifestyle, there are a few cards you absolutely can’t function without. These aren’t just conveniences—they’re non-negotiables that help you get paid, ride the metro, open a bank account, access healthcare, and even prove your identity in the UAE.

From the Emirates ID (the UAE’s national identity card) to bank debit and credit cards, Nol cards for public transport, and the new Jaywan card—each one plays a different role in your day-to-day life. If you’re not sure what these cards are, why you need them, or how to get them, this guide breaks it all down for you, step-by-step.

We’re also covering the latest updates for 2025, including digital options, card-linked rewards, and multi-currency travel cards. So whether you’re fresh off the plane or in your second year here, this article will help you stay informed and card-ready.

By the end of this guide, you’ll know:

- Which 5 cards every expat needs in Dubai

- How to apply for them and what documents are required

- The difference between cards like Jaywan, Nol, and standard bank cards

- Tips to choose the best options for your needs (especially if you’re new to the UAE)

Let’s make settling in smoother, smarter, and stress-free. These cards aren’t just plastic—they’re your gateway to life in Dubai.

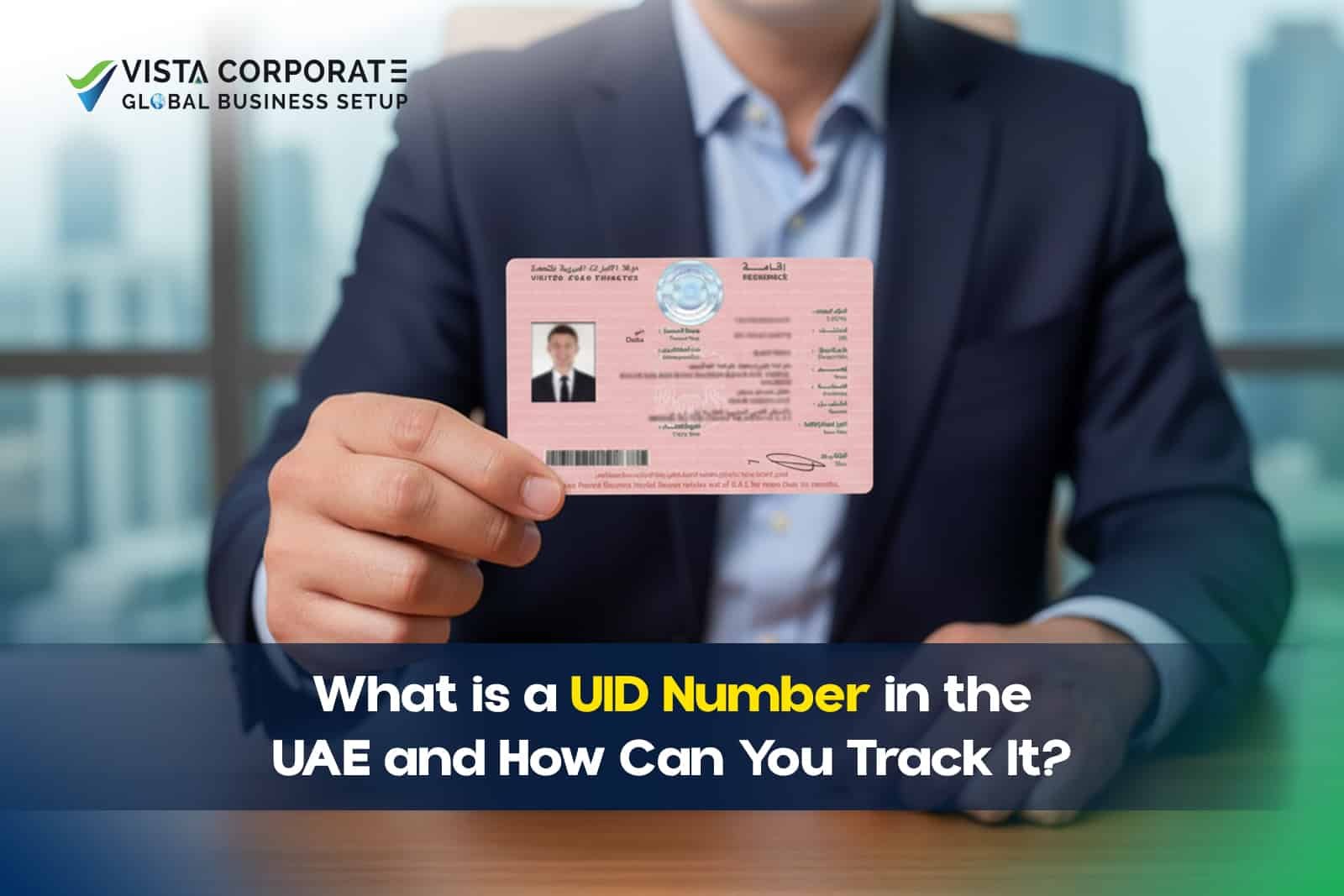

1. Emirates ID – Your Primary Identity as a Dubai Expat

If you’re living in Dubai, there’s one card that defines your legal identity—the Emirates ID. Whether you’re applying for a phone number, opening a bank account, or checking in at immigration, this card is your official all-access pass. It’s more than just an ID—it’s a smart chip-based national identity card issued by the Federal Authority for Identity, Citizenship, Customs & Port Security (ICP), and it’s mandatory for all UAE residents, including expats.

You’ll need your Emirates ID to:

- Sign rental agreements

- Open a bank account

- Apply for mobile or internet services

- Get access to healthcare services

- Link to digital services like the UAE Pass app

- Use as an official ID instead of your passport for many local services

This card comes with a unique 15-digit identification number, your personal data, and biometric details such as fingerprints and a facial scan. It’s used across both private and public sector systems to authenticate your identity.

How to Apply for an Emirates ID as an Expat in Dubai

Applying for an Emirates ID is tied directly to your residency visa process. Whether you’re employed or running your own business, here’s how it typically works:

Step-by-Step Process:

- Apply via ICP or a typing center

- You’ll need a copy of your passport, UAE entry permit, passport-size photos, and visa application forms.

- You’ll need a copy of your passport, UAE entry permit, passport-size photos, and visa application forms.

- Undergo a medical fitness test

- This includes a blood test and chest X-ray. Required for first-time applicants and renewals.

- This includes a blood test and chest X-ray. Required for first-time applicants and renewals.

- Submit biometric data

- First-timers must visit an authorized center for fingerprinting and a photograph.

- First-timers must visit an authorized center for fingerprinting and a photograph.

- Track your application

- Use the ICP’s official portal or UAE Pass app to check Emirates ID application status.

- Use the ICP’s official portal or UAE Pass app to check Emirates ID application status.

- Receive your ID

- Once approved, your card will be available for collection at the post office you selected or delivered to your location.

- Once approved, your card will be available for collection at the post office you selected or delivered to your location.

Most employers or PRO services assist with the entire process, but it’s still helpful to understand how it works.

Lost, Expired, or Damaged Emirates ID? Here’s What to Do

Misplaced your Emirates ID? First, don’t panic. Then follow this:

- Report it immediately to ICP through their online portal or at the nearest Customer Happiness Center.

- Pay the replacement fee and request a new card.

- For expired IDs, start your renewal process 30 days before expiration. You’ll receive reminders via SMS.

Pro tip: Never delay updating or renewing your Emirates ID. It’s tied to your visa status, your banking privileges, and even your health insurance access.

The Emirates ID is non-negotiable for expats in Dubai. Without it, you’re basically invisible in the system. It’s the first and most crucial card you need—everything else follows after.

2. Bank Cards – Opening an Expat-Friendly Bank Account in Dubai

After getting your Emirates ID, your next essential step as an expat is to open a bank account in the UAE. This unlocks everything—from getting your salary to managing bills, subscriptions, investments, and travel expenses. Once your account is set up, you’ll receive either a debit card, credit card, or both, depending on your eligibility and preferences.

Dubai has a well-regulated banking system, and many banks here cater specifically to expats. But it’s important to understand the options and choose a bank that fits your lifestyle, visa type, and income structure.

How to Open a Bank Account in Dubai as an Expat

Most banks in the UAE require you to be a resident with a valid visa and Emirates ID to open a personal account. Here’s a simple guide to how it’s usually done:

Required Documents:

- Emirates ID (or Emirates ID application form if it’s in process)

- Valid residence visa

- Passport with a stamped visa page

- Salary certificate or offer letter (if you’re employed)

- Tenancy contract or utility bill (sometimes requested for address proof)

Some banks also request:

- A letter from your employer or sponsor

- Your latest bank statements (if transferring from another UAE account)

Steps to Open an Account:

- Choose the bank that best suits your needs (covered in the next subheading).

- Visit the branch or apply online. Many banks now allow digital onboarding.

- Submit the documents.

- Undergo identity verification.

- Receive your debit card and checkbook within a few business days.

Once your account is active, you can apply for additional services like credit cards, overdraft facilities, or multi-currency accounts.

Debit vs. Credit Cards – Which is Better for Expats in Dubai?

Here’s a quick breakdown of how debit cards and credit cards differ for expats:

| Feature | Debit Card | Credit Card |

| Funds Source | Directly from your bank balance | Borrowed funds from the bank |

| Eligibility | Immediate with most personal accounts | Requires income proof and credit check |

| Common Uses | Groceries, ATM withdrawals, utility bills | Travel, shopping, large purchases |

| Risk of Overspending | Low | Higher (especially for new expats) |

| Perks | Limited | Cashback, air miles, lounge access, etc. |

As an expat, start with a debit card, especially if you’re new and still getting financially settled. Once you’ve built a stable income track and have a good relationship with the bank, you can consider applying for a credit card to enjoy added benefits.

Best Banks for Expats in Dubai (2025 Edition)

Here are some top banks that are known for being expat-friendly in the UAE:

- HSBC UAE: Global access, great for UK/Asian expats, digital banking tools.

Keywords: HSBC expat credit card Dubai eligibility, virtual bank account Dubai expat - Mashreq Bank: Fast onboarding, flexible account types, known for Mashreq Neo (digital-only).

Keywords: Mashreq credit card advantages expats - Emirates NBD: Strong local presence, digital account openings, the “Go4It” card with Nol card integration.

Keywords: Emirates NBD go for it card expat perks - Citi UAE: Offers one of the best cashback credit cards. Great for frequent travelers.

Keywords: Citi cashback credit card for UAE expats - RAKBANK: Known for its RTA Nol linked credit cards and good digital service support.

Keywords: Rakbank RTA Nol linked card expats - FAB (First Abu Dhabi Bank): Preferred for high-income expats, offers great multi-currency solutions.

Each of these banks has different eligibility criteria, benefits, and card options. Make sure to compare features like online banking tools, reward points, and global ATM access before choosing.

Bank cards are your daily drivers in Dubai. Whether you’re paying rent, dining out, or shopping online, you’ll need a reliable card backed by a secure bank. Start simple, then build toward more advanced services like multi-currency cards, expat travel rewards, and credit card perks.

3. Nol Card – The Must-Have Transit Card for Expats

Dubai has one of the most advanced and well-connected public transport systems in the world—and to use it efficiently, you’ll need a Nol Card. Whether you’re hopping on the Metro, catching a bus, paying for parking, or even taking a water taxi, the Nol Card is your essential travel companion.

Issued by the Roads and Transport Authority (RTA), this contactless smart card lets you pay for multiple modes of transport and services across the city. It’s reloadable, easy to use, and even comes with loyalty perks like Nol Plus rewards, making it a must-have for any expat navigating Dubai.

Why Every Expat Needs a Nol Card

If you’re an expat without a car, or you simply prefer Dubai’s clean and air-conditioned public transit, the Nol Card is non-negotiable. But even if you drive, the card is still necessary for:

- Paying for RTA parking across the city

- Riding the Metro (Red & Green Lines)

- Taking buses or feeder buses

- Using water buses or trams

- Buying entry tickets at some museums and public parks

The Nol Card also connects to other systems like Dubai’s RTA journey planner, making it super easy to plan your daily commute.

Types of Nol Cards – Which One Should Expats Choose?

RTA currently offers different types of Nol Cards, each catering to specific needs. Here’s a breakdown:

| Card Type | Best For | Valid For | Special Notes |

| Silver Card | Regular commuters | Metro, Bus, Tram, Parking, Water Bus | Most popular; valid for 5 years |

| Gold Card | VIP travel experience | Same as Silver + Access to Gold Cabins | Slightly higher fare; VIP metro cabin access |

| Red Ticket | Tourists or occasional riders | Short-term use on Metro, Tram, Bus | Valid for up to 10 trips or 5 daily passes |

| Blue Card | Residents who want personalisation | All transport services | Linked to Emirates ID; supports auto top-up |

For most expats, the Silver Card is the best starting point. If you commute daily and value comfort, upgrade to Gold. Long-term residents can personalize their Blue Card, which includes added security and can be replaced if lost.

How to Get and Top-Up Your Nol Card

Getting your card is simple:

- Visit any Metro station, RTA Customer Happiness Centre, bus terminal, or selected grocery stores.

- You can also purchase and manage cards through the RTA Dubai app or official website.

Top-up options:

- Recharge online (via the RTA website or Nol app)

- Use ticket vending machines at Metro and bus stations

- Enable auto top-up via linked credit/debit cards (only for Blue Cards)

- Pay with Apple Pay or Samsung Pay at RTA counters

Bonus Tip: If you link your Nol card with your Emirates ID or a credit card like RAKBANK’s Nol credit card, you can enjoy additional rewards or streamlined payments.

The Nol Card is more than just a ticket to get from point A to point B—it’s a smart way to manage your travel in Dubai. For expats, especially new arrivals, this little card brings big convenience.

4. Jaywan Card – UAE’s National Debit Payment Solution for Expats

The Jaywan Card is the UAE’s bold step toward building a fully integrated national payment system—and as an expat in Dubai, it’s something you’ll likely encounter soon, if you haven’t already. This domestic debit card initiative is designed to streamline transactions, improve security, and reduce reliance on foreign card networks like Visa or Mastercard within the UAE.

What makes Jaywan different?

It’s part of the UAE’s national switch system known as “JomPAY” and is backed by the Central Bank of the UAE. The card is built on the RuPay platform (yes, the same one that powers India’s national payment infrastructure) and is being gradually rolled out through local banks, offering expats and residents an alternative to international debit cards for domestic purchases and bill payments.

Why the Jaywan Card Matters for Expats in Dubai

As an expat, you may wonder: “Why get a Jaywan Card when I already have a Visa or Mastercard debit card?” Here’s why:

- Locally optimized for use at all ATMs, PoS systems, and digital platforms in the UAE.

- More secure due to real-time monitoring and in-country data hosting.

- Faster settlement of payments for local businesses and merchants.

- Future integration with digital wallets and services like AANI (UAE’s instant payment platform).

- Encourages wider acceptance among government services, toll payments, utility bills, and mobile recharge.

Jaywan is also being promoted as a cost-effective and secure alternative for day-to-day spending—without fees from foreign card networks for local transactions.

Keywords naturally included here: Jaywan card UAE expats, Jaywan debit card rollout UAE, Jaywan vs Visa Mastercard in UAE, instant payment platform AANI UAE cards.

Eligibility and How to Get a Jaywan Card in Dubai

The Jaywan card is available to both UAE nationals and expat residents. However, it’s important to note that the card is issued only through selected UAE banks (for now), and not all banks have adopted it yet.

Here’s how to get one:

- Open a bank account with a participating bank (e.g., Emirates NBD, Mashreq, FAB, RAKBANK).

- Choose Jaywan as your preferred debit card option (if available).

- Verify your Emirates ID and residence visa—required to issue the card.

- Once issued, link it with your mobile wallet, e-commerce accounts, or loyalty programs.

Currently, Jaywan cards are offered co-branded with either Visa or Mastercard, ensuring broader usability while maintaining the benefits of local infrastructure.

Benefits of the Jaywan Card for Expats

| Feature | Jaywan Card Benefit |

| Domestic Spending | Zero international gateway charges on local transactions |

| Government Integration | Can be used to pay for services at ICA, MOHRE, RTA, and utility portals |

| Local Data Hosting | Improved security, faster fraud detection |

| Seamless Retail Use | Works across supermarkets, fuel stations, malls, and service centers |

| Compatibility | Upcoming support for AANI instant payments and mobile wallets |

In short, Jaywan is tailored for UAE life, and as it gains traction, it’s set to become the standard debit card for all daily spending within the country. As an expat, having a Jaywan card makes you future-ready and helps you align with the UAE’s financial ecosystem.

5. Credit Cards with Expat Perks (Cashback, Travel, and More)

When you’re living in Dubai, a credit card isn’t just a payment tool—it’s a financial asset that can unlock travel benefits, cashback on groceries and fuel, access to airport lounges, and even help you build credit history in the UAE. For expats, choosing the right credit card can be a game-changer, especially when used responsibly.

Most UAE banks offer tailored credit card solutions for expats, including cards linked with Emirates Skywards, Noon shopping vouchers, or Nol travel cards. Some come with lifestyle perks, while others are travel-heavy. But eligibility depends on your income, visa type, and in some cases, your employment status.

Top Credit Cards in Dubai for Expats in 2025

Here are some of the most expat-friendly credit cards available in Dubai this year, each offering a unique blend of rewards and lifestyle features:

| Credit Card | Ideal For | Key Features |

| Citi Cashback Card | Everyday spenders | Cashback on groceries, fuel, and online shopping |

| Emirates NBD Go4It Card | Public transport users | Combines Nol card + cashback + metro access |

| HSBC Platinum Credit Card | Frequent flyers & expats with savings | Air miles, airport lounge access, no annual fee |

| Mashreq Platinum Elite Credit Card | Lifestyle-focused expats | Rewards on dining, entertainment, and shopping |

| Standard Chartered Manhattan Platinum | Salary-based perks seekers | Monthly cashback tied to salary transfer and spending goals |

| RAKBANK Titanium Credit Card | Budget-conscious expats | Low forex fees, cashback, and RTA integration |

These cards often come with welcome bonuses, travel insurance, purchase protection, and extended warranty coverage. Some even offer multi-currency billing, which is great if you’re frequently moving funds between countries.

Eligibility & Salary Requirements for Expat Credit Cards

To get approved for a credit card in Dubai, most banks ask for a minimum monthly salary and a valid residence visa. Here’s a general idea of what you’ll need:

Basic eligibility requirements:

- Valid Emirates ID

- UAE residence visa

- A salary certificate from your employer or company

- Bank statement (last 3–6 months)

- Proof of address (tenancy contract, utility bill)

Some cards—especially premium ones—might require:

- A higher income bracket

- Employment in select companies or government sectors

- A credit score, if you’ve already held financial products in the UAE

Pro tip: If you’re self-employed, you may need to provide your trade license or proof of income from your business.

Multi-Currency and Travel-Friendly Credit Cards for Expats

Dubai is a global hub, and many expats send money back home or travel across the GCC, India, Europe, or Southeast Asia. That’s why multi-currency credit cards are gaining popularity. They allow you to:

- Spend in various currencies without conversion losses

- Avoid foreign transaction fees on global websites or POS systems

- Track spending per currency for better budgeting

Some cards also offer airline miles, hotel points, or direct benefits with travel portals like Booking.com and Agoda. Look out for:

- Airport lounge access via LoungeKey or Priority Pass

- Complimentary travel insurance

- Flight ticket discounts or upgrades

If you’re an Indian expat, UK national, or a global professional, these cards can offer huge value, especially when compared to using your home country card overseas.

Whether you’re shopping, commuting, or jet-setting, having the right credit card adds comfort and value to your expat life in Dubai. Choose based on your lifestyle, not just the flashiest reward program.

Bonus: Health Card – Do Expats Need One in Addition to Emirates ID?

This one’s a common question among expats who are new to Dubai: “If I already have an Emirates ID, do I still need a separate health card?” The short answer is: it depends on where you plan to receive medical care.

Your Emirates ID today is integrated with most private and public services—including some aspects of healthcare. However, certain government health facilities still require a dedicated Health Card issued by the Dubai Health Authority (DHA) or Ministry of Health and Prevention (MOHAP), depending on your location within the UAE.

What Is a Health Card?

A Health Card is a physical card that gives you access to government hospitals and clinics at subsidized rates. It’s especially helpful if:

- You don’t have private health insurance

- Your employer only provides a basic plan

- You want treatment at DHA-run facilities like Rashid Hospital, Latifa Hospital, or Al Barsha Health Centre

While some of these services are linked to your Emirates ID, others still require the card as proof for registration or walk-ins.

How to Get a Health Card in Dubai

You can apply for a Health Card online via the DHA website or visit a DHA medical fitness center.

Documents typically required:

- Emirates ID

- Passport copy

- Visa page copy

- Passport-size photograph

- Proof of address or tenancy contract (sometimes requested)

After your application is approved, you’ll receive a digital or physical card that’s valid for one year and renewable.

Pro tip: Even if you don’t plan to use it often, having a Health Card can act as a backup if your insurance doesn’t cover a specific treatment or you want quick access to government facilities.

Is It Mandatory?

No, not for everyone. If you already have a comprehensive private health insurance plan—which is mandatory in Dubai—you may never need to use the Health Card. But for certain jobs (especially domestic workers or blue-collar roles), the Health Card is a key access pass to medical services.

Think of the Health Card as your healthcare safety net. It’s not a must-have for every expat, but it’s definitely a smart card to consider—especially if you want access to government healthcare without surprises.

Things to Keep in Mind Before Applying for Any Card in Dubai

Before you rush to collect all the cards we’ve talked about—Emirates ID, Nol, Jaywan, credit or bank cards—pause and plan smart. While Dubai is welcoming and highly digital, card issuance processes still depend on legal status, documentation, and sometimes even banking relationships. Whether you’re a fresh arrival or a long-term expat, these important reminders can save you time, paperwork headaches, and delays.

1. Make Sure Your Residency Is Active and Updated

Your Emirates ID and UAE residence visa are the keys to unlocking almost every card and service in Dubai. Most banks, telecom companies, and government services will ask for both.

- Your Emirates ID must be valid—not expired or under processing—to apply for most bank and credit cards.

- Nol and Jaywan may not require full residency, but having your ID linked to them improves convenience.

- For new arrivals, some services might allow applications using Emirates ID application forms temporarily.

2. Understand What’s Linked to Your Emirates ID

Several cards and services are now directly integrated with your Emirates ID:

- Bank accounts link your ID to your profile for identity verification and KYC compliance.

- RTA Nol Blue cards are personalized and can be tied to your Emirates ID for easy recharge and tracking.

- Jaywan cards require your Emirates ID for issuance and activation.

- Government portals like ICA, MOHRE, and DHA are connected to your ID for healthcare, visa renewals, and fines.

Tip: If you renew your Emirates ID or get a new number, update it across all your accounts and service providers.

3. Know the Digital vs Physical Card Options

Dubai is rapidly adopting digital-first solutions. Some banks and government agencies now offer virtual cards that work through apps or wallets like Apple Pay and Samsung Pay.

- Mashreq Neo, Liv. by Emirates NBD, and YAP are popular digital banks for expats that issue virtual cards instantly.

- Nol card top-ups and usage can be fully managed through RTA apps.

- Jaywan will soon be integrated into UAE’s digital payment platforms like AANI, enhancing instant transfers without the need for physical cards.

Still, having physical versions of cards like Emirates ID or your main debit card is essential for many offline services and formal verifications.

4. Double-Check Your Eligibility Before Applying

Before applying for any card, review:

- Salary or income requirements (especially for credit cards)

- Document checklist (some banks ask for tenancy contracts or salary slips)

- Processing times (some cards are issued instantly; others take days)

- Annual fees or usage terms (even if we’re not discussing exact costs, conditions do apply)

If unsure, visit the bank’s or government agency’s official website, or get help from a trusted business setup consultant, PRO, or relocation service.

5. Stay Alert for Future Integrations

Dubai is constantly evolving, and the ecosystem of expat cards is moving toward centralized digital identity and payments. Keep an eye on:

- AANI: UAE’s instant transfer system that’s expected to replace conventional money transfer modes.

- Digital ID apps like UAE Pass, which may soon replace the need to carry multiple physical cards.

Quick Table – Top 5 Must-Have Cards for Expats in Dubai (2025)

Whether you’re in your first week or fifth year in Dubai, having the right set of cards helps you navigate daily life, legal systems, and financial services with ease. Here’s a quick snapshot of the top 5 cards every expat in Dubai should have—and why each one matters.

| Card Type | Primary Use | Issuing Authority | Linked to Emirates ID | Key Benefits for Expats |

| Emirates ID | Official identity, government services | Federal Authority (ICP) | N/A | Legal requirement, opens access to all public/private services |

| Bank Debit Card | Salary deposits, daily spending | UAE Banks (e.g., NBD, Mashreq) | ✅ | ATM access, bill payments, e-commerce, mobile wallets |

| Nol Card | Metro, bus, parking, tram, water taxi | RTA (Roads & Transport Authority) | Optional | Affordable, fast public transit, loyalty rewards (Nol Plus) |

| Jaywan Card | Domestic payments, government services | UAE Banks (Jaywan platform) | ✅ | Fast, secure, UAE-only payments, integrated with local systems |

| Credit Card | Travel, shopping, cashback perks | UAE Banks (HSBC, Citi, etc.) | ✅ | Lounge access, travel insurance, shopping rewards, multi-currency |

✅ Why This Table Matters

Use this table to evaluate:

- What cards you already have

- What you still need to apply for

- Which ones are tied to your Emirates ID

- How each card supports a different aspect of expat life in the UAE

Each of these cards complements the others. Together, they help you live legally, spend smartly, travel easily, and build financial credibility while living in Dubai.

Final Thoughts – Stay Card-Ready as a Dubai Expat

Living in Dubai as an expat comes with endless opportunities—but also a learning curve. From riding the Metro to setting up your bank account or accessing healthcare, the right set of cards makes everything smoother. These aren’t just plastic—they’re part of how the city recognizes, processes, and serves you as a resident.

Here’s a quick recap of what we covered:

- The Emirates ID is the foundation of your identity and access to government systems.

- A bank debit card is your go-to for everyday expenses and salary deposits.

- The Nol Card helps you move across the city—affordably and efficiently.

- The Jaywan Card positions you within the UAE’s evolving local payments ecosystem.

- A good credit card opens doors to rewards, travel perks, and financial flexibility.

And while these five are must-haves, others like the Health Card, multi-currency cards, and digital banking tools can help round out your toolkit for living smart in Dubai.

As Dubai moves further into digital services, real-time payments, and integrated ID systems, staying updated on card-related developments is essential. If you ever feel unsure about what’s required, check with your employer, PRO service, or local bank—they’ve likely guided thousands of expats before you.

One last tip:

Always review your cards every year. Check expiry dates, card limits, linked services, and whether you’re still getting the benefits you signed up for.

FAQs – Everything You Want to Know About Expat Cards in Dubai

What are the top 5 essential cards every expat needs in Dubai?

The top 5 essential cards for expats in Dubai include:

- Emirates ID – Your legal ID for all government, financial, and healthcare transactions.

- Bank Debit Card – For salary deposits, daily spending, and ATM withdrawals.

- Nol Card – For public transport including metro, buses, water taxis, and parking.

- Jaywan Card – The UAE’s domestic debit card linked to the national payment system.

- Credit Card – For added financial flexibility, travel benefits, and rewards.

These cards ensure access to core services and simplify everyday tasks. While optional cards like a health card or multi-currency card add convenience, the five listed above are must-haves for living legally and comfortably in Dubai.

Is Emirates ID mandatory for expats in the UAE?

Yes, the Emirates ID is mandatory for all residents of the UAE, including expats. Issued by the Federal Authority for Identity, Citizenship, Customs & Port Security (ICP), it acts as your primary identification document.

Without it, you cannot:

- Open a bank account

- Sign a lease or tenancy contract

- Apply for mobile services or internet

- Access government health or legal services

New residents must apply for the Emirates ID during their residency visa process. It’s tied to your biometric data, used for security, and must be carried at all times. Even renewing your driver’s license or paying fines involves this ID.

Which bank cards are best for expats in Dubai in 2025?

Top bank cards for expats in 2025 include:

- HSBC Platinum – Ideal for global professionals with travel perks.

- Mashreq Neo – A digital-first card for tech-savvy users.

- Emirates NBD Go4It – Combines Nol access with banking features.

- Citi Cashback – Great for saving on groceries, fuel, and online shopping.

- RAKBANK Titanium – Low foreign exchange rates and RTA-linked benefits.

Choose a card based on your spending habits, travel needs, and income level. Many offer no-fee options, cashback programs, and international acceptance—crucial for expats with cross-border financial commitments.

How can an expat apply for an Emirates ID in Dubai?

To apply for an Emirates ID as an expat, follow these steps:

- Visit an ICP typing center or apply via the ICP website.

- Submit required documents: passport, residence visa, photo, and application form.

- Undergo a medical fitness test at an approved center.

- Complete biometric registration (fingerprints, photo) at an authorized facility.

- Wait for application processing and approval (check status via ICP portal).

- Collect the card at the selected post office or opt for delivery.

The ID is usually valid for 1–3 years depending on your visa. Always keep it updated and renew it before expiration to avoid fines or service disruption.

What are the benefits of having a multi-currency card in the UAE?

Multi-currency cards are highly beneficial for expats in Dubai, especially those who:

- Travel frequently across the GCC, Asia, or Europe.

- Send money home or receive funds in foreign currencies.

- Shop online in USD, GBP, EUR, etc.

Benefits include:

- No currency conversion fees

- Real-time FX locking for predictable rates

- Easier budgeting across currencies

- ATM access worldwide in local currency

Some banks also offer multi-currency wallets within a single card or app. This feature is ideal for freelancers, digital nomads, and business owners dealing with clients across borders.

Can expats get credit cards in Dubai without a salary certificate?

Generally, a salary certificate is required to get a credit card in Dubai. However, there are exceptions:

- Self-employed expats can use their trade license and income proof.

- Some digital banks may accept bank statements instead.

- A few secured credit cards require a fixed deposit instead of a salary.

Still, most traditional banks prefer a minimum income threshold with official salary documentation. Speak with your bank about alternative eligibility routes if you’re newly employed, a freelancer, or business owner.

What documents are required to get a bank account in Dubai for expats?

To open a bank account in Dubai as an expat, you’ll typically need:

- Valid Emirates ID

- UAE residence visa

- Passport with stamped visa page

- Salary certificate or proof of employment

- Tenancy contract or utility bill for address proof

- Sometimes, recent bank statements

Requirements vary slightly by bank. Some offer simplified onboarding for salaried employees, while others may ask for additional documents if you’re self-employed or applying for premium banking services.

Are there any prepaid cards recommended for new expats in Dubai?

Yes, prepaid cards are great for new expats who haven’t yet opened a bank account or are awaiting their Emirates ID. Options include:

- Noon Pay Card

- Careem Pay Card

- YAP Digital Card

- UAE Exchange Cards

Benefits:

- No minimum income or employment requirement

- Reloadable via app or kiosks

- Usable for shopping, bill payments, or online services

- Great for budgeting and safety

Prepaid cards are instant, secure, and widely accepted—making them a smart short-term tool for newcomers.

Which travel cards are best for frequent flyers living in Dubai?

Top travel-friendly credit cards for expats include:

- Emirates Skywards Cards (Emirates NBD, Citibank)

- HSBC Premier World Elite

- Standard Chartered Visa Infinite

- ADCB Traveller Credit Card

Perks:

- Air miles on every spend

- LoungeKey access across global airports

- Travel insurance and hotel discounts

- Multi-currency spending

Choose cards that align with your preferred airline and travel frequency. These cards help expats turn daily spending into free flights and VIP travel experiences.

What’s the difference between Emirates ID and UAE Residence Visa?

The UAE Residence Visa is stamped in your passport and shows your legal permission to live in the country. The Emirates ID, on the other hand, is a smart identity card issued after your visa is approved.

Key differences:

- Residence Visa: Linked to your employer, company, or property

- Emirates ID: Used for all interactions in the UAE (banking, health, etc.)

While the visa grants entry and residency, the Emirates ID is your daily proof of identity inside the UAE. Both are interlinked and equally important.

How long does it take to receive your Emirates ID after application?

Once your Emirates ID application is submitted and approved, the typical timeline for receiving your card is 5 to 10 working days. However, the exact duration depends on:

- Completion of medical fitness test and biometrics

- Processing time at the ICP (Federal Authority for Identity and Citizenship)

- Whether you opted for standard or express delivery

- Current application volumes (may vary during peak relocation seasons)

You can track the status on the ICP portal using your application number. Once ready, the card is either delivered to your chosen post office or sent directly to your residence if selected.

What are the charges for maintaining bank cards in Dubai?

While exact fees vary by bank and card type, you should be aware of common charges associated with bank cards:

- Annual maintenance fees (waived for salary-linked accounts)

- ATM withdrawal fees (especially if using another bank’s ATM)

- Foreign transaction fees

- Card replacement charges

- Late payment or over-limit fees (for credit cards)

Some banks waive these fees if you meet minimum balance or monthly spend criteria. Always read the terms and conditions to understand how your usage affects these charges.

Can tourists apply for any of these essential cards in the UAE?

Most of the must-have cards discussed (like Emirates ID, bank cards, and credit cards) are restricted to residents only. However, tourists can apply for:

- Nol Card (Red Ticket or Silver) for transport

- Prepaid travel cards for currency exchange and spending

- Visitor SIMs that may offer temporary virtual cards

Since Emirates ID and Jaywan are tied to residency status, tourists are not eligible. For short stays, bring international cards or get a prepaid travel card from local exchanges or digital platforms.

Which digital banks in Dubai offer cards for expats?

Several digital-only banks in the UAE offer cards tailored for expats:

- Liv. by Emirates NBD

- Mashreq Neo

- YAP

- Zand (soon-to-launch full-stack digital bank)

Features include:

- Instant digital card issuance

- No physical branch visits

- Low documentation requirements

- Seamless in-app card management

These digital banks are perfect for expats looking for mobile-first experiences and fast onboarding. Most issue virtual debit cards linked to your UAE phone number and Emirates ID.

Is it better to get a local UAE bank card or use an international one?

For expats, local UAE bank cards are a better choice for everyday living. Here’s why:

- No foreign exchange or cross-border transaction fees

- Easy salary deposits and direct debit for bills

- Widely accepted across government services and utilities

- Easier access to credit, loans, and loyalty programs

International cards are good for backup, but long-term usage in Dubai may incur currency conversion costs and international ATM charges. Local cards integrate better with services like Nol, Jaywan, and UAE Pass.

Are expats eligible for cashback or reward cards in Dubai?

Yes, expats are eligible for a wide range of cashback, rewards, and lifestyle benefit cards offered by UAE banks. In fact, many cards are tailored specifically for expat spending patterns, with perks like:

- Cashback on groceries, fuel, and utility bills

- Rewards points redeemable for flights, hotels, and shopping

- Airport lounge access

- Dining discounts and movie offers

Eligibility depends on income, credit history, and sometimes your employer. Cards like Citi Cashback, HSBC Platinum, and Mashreq Cashback are top choices among expats in 2025.

Do all banks in Dubai require a residence visa for card issuance?

Yes, for most financial products, including debit and credit cards, banks in Dubai require a valid UAE residence visa. Exceptions may include:

- Prepaid cards that do not require full KYC

- Digital accounts opened with a passport and Emirates ID application

However, for full-featured cards like credit cards or current accounts, residency proof is essential. The residence visa validates your legal stay, employer, and eligibility for financial services.

Can I use my home country credit card in Dubai malls and ATMs?

Yes, international credit cards (Visa, Mastercard, Amex) are widely accepted across:

- Malls

- Restaurants

- Hotels

- Supermarkets

- Online portals

You can also use them at ATMs. However, keep in mind:

- Foreign transaction fees may apply

- Dynamic currency conversion could cost more

- Some services (like utility payments or Nol recharge) prefer UAE-issued cards

International cards are great for tourists or short visits, but residents should switch to UAE cards for better rates and compatibility.

What to do if your Emirates ID is lost or expired as an expat?

If your Emirates ID is lost, stolen, or damaged, follow these steps:

- Report the incident to the ICA or nearest Customer Happiness Center.

- Pay the replacement fee and fill out the application online or via typing center.

- Revisit for biometrics if required.

- Track application status and collect your new ID or have it delivered.

For expired IDs, begin the renewal process 30 days before the expiration date. Delays may result in fines and disruption of services like banking, telecom, or insurance.

Do expats need a separate health card in addition to Emirates ID?

Not necessarily. If you have private health insurance, your Emirates ID is often enough to access healthcare services.

However, if you plan to use government hospitals or clinics, you may still need to:

- Apply for a Dubai Health Authority (DHA) card

- Register through MOHAP if residing outside Dubai

Some medical services—especially in public facilities—still require the Health Card for subsidized rates. It’s not compulsory, but a good backup if your insurance is limited or not yet active.

Search

Recent Post